The House of Representatives recently passed the Tax Relief for American Families and Workers Act of 2024. The bill includes provisions that would extend immediate expensing for research and development and short-lived assets including vehicles, machinery, and other equipment through 2025 and 2026, respectively.

Immediate expensing is beneficial for American competitiveness, innovation, and economic opportunity. Expensing is also good for the environment because it spurs investment in more energy-efficient equipment, clean energy technologies, and U.S companies that have an environmental advantage.

While the Tax Relief for American Families and Workers Act of 2024 makes important fixes to the tax on expensing, businesses would benefit from more certainty by making expensing provisions permanent.

What is Expensing and What is the Current Policy?

Immediate expensing, also commonly known as bonus depreciation, refers to the practice of allowing businesses to deduct the full cost of qualifying capital expenditures from their taxable income in the year the expenses are incurred. With traditional depreciation schedules, businesses must deduct the cost of investments over time, which can range from a few years to 39 years depending on the asset.

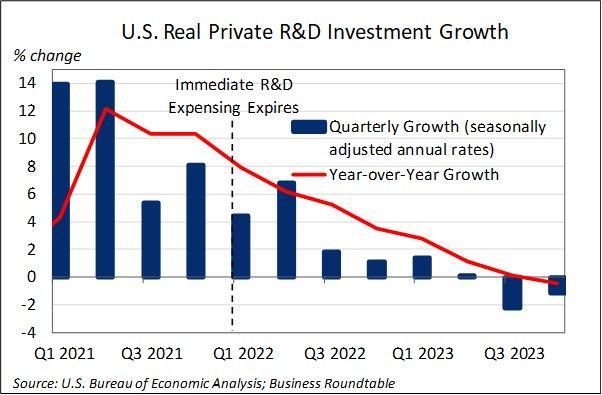

For roughly 70 years, businesses could fully deduct expenses in basic and applied research and development in the first year. The provision covered everything from the scientists and entrepreneurs conducting the research to the cost of equipment and facilities. It also included domestic and foreign R&D investments. That provision lapsed in 2022, meaning companies would have to amortize the expenses over five years. For research occurring outside the country, expenses must be amortized over fifteen years. As the National Association for Manufacturers emphasizes, the U.S. is now only one of two developed countries in the world to require amortization of R&D expenses. And the policy lapse puts the U.S. at an even further disadvantage compared to the way China treats R&D expensing. Chinese policy provides a super deduction, allowing a company to immediately deduct twice the amount of R&D spending (an additional 100 percent).

It works like this: In a world with immediate expensing, if a company has $2 million in income, but $1 million in R&D expenses, the firm’s taxable income would be $1 million (after fully deducting the $1 million). Under the new provisions, the company could only deduct $100,000 in the first year, making the taxable income for the year $1.9 million.

The lapsing of immediate expensing for R&D has already created a notable decrease in R&D investment. A recent Chamber of Commerce analysis found that “rate of growth of R&D spending has declined from 6.6% on average over the previous five years to less than 1% over the last 12 months—notably decreasing by 1.2% in the most recent quarter.” Without a fix, the R&D Coalition projects that the U.S. economy would see a drop in R&D spending by more than $4 billion annually in the first five years and $10 billion annually over the second five. Within a decade, more than 50,000 jobs would be lost.

Depreciation schedules for other investments depend on the asset. Equipment, vehicles, and machinery could be anywhere from 3 years to 20 years while commercial property is 39 years. Bonus depreciation has existed in certain percentages (including zero when policies lapsed) since 2002, and both Republican and Democrat administrations have espoused the benefits of expensing. The Tax Cuts and Jobs Act of 2017 made the most recent changes, enacting 100 bonus depreciation or full expensing for assets purchased and placed in service from September 2017 through 2022. Expensing phased down 20 percent per year beginning in 2023, fully phasing out beginning in 2027.

The Environmental Benefits of Immediate Expensing

There are several environmental benefits to immediate expensing. They include:

- Greater energy efficiency and capital stock turnover. Expensing incentivizes energy- and water-efficient investments. Those investments could include an HVAC system, more energy efficient lighting, water heaters, insulation, or a new piece of farm equipment that uses less fuel. Companies that have fleets for transportation can invest in more energy efficient or alternative-fuel technologies for cars, trucks, and planes. Expensing for energy efficiency is a win-win-win scenario because it reduces the cost of the initial investment, it saves businesses money on their energy and water bills, and it reduces emissions.

- Accelerating innovation. Immediate expensing is essential for firms of all sizes but can particularly be beneficial to start-ups and small businesses. Energy startups allot a greater percentage of their spending on R&D and sometimes must operate on thin margins or at a loss for years before becoming profitable. Immediate expensing accelerates the return on investment for businesses and startups. Whether it is advanced nuclear, geothermal, solar cells, or batteries, immediate expensing is pivotal for clean energy startups and moving from concept to deployment. According to the U.S. Chamber of Commerce, 29 percent of small businesses take advantage of R&D expensing, and 45 percent of small business tech companies do. This includes many climate tech companies that aim to provide power, transportation, and products with fewer emissions and a smaller environmental footprint. Immediate expensing for R&D and short-lived assets can help accelerate the growth of environmentally friendly technologies and help make them financially viable in the long run.

- Leveraging America’s environmental advantage. The overall impact of immediate expensing on emissions is hard to measure because it could lead to higher levels of economic growth, more investment in capital intensive energy and manufacturing, and therefore higher levels of consumption. If the U.S. cedes ground because of uncompetitive policies, however, it could be costly for American jobs, the economy, and the environment. The United States has a carbon advantage when it comes to many manufacturing processes, as well as the production of oil and natural gas (including offshore). If production and manufacturing shifts to countries where the environmental standards are less rigorous, global emissions would be higher than they otherwise might be. Further, the environmental benefits of immediate expensing are not limited to the development of cleaner technologies; they extend to the broader economy. A shift toward sustainable practices can often involve upfront costs, and immediate expensing helps businesses recoup these expenses rapidly. This, in turn, encourages widespread adoption of environmentally friendly practices, creating a ripple effect throughout supply chains and industries. In effect, immediate expensing can help countries decouple economic growth and emissions and help emerging countries adopt cost-competitive, cleaner technologies that also raise standards of living.

Fixing the Problem of Policy Uncertainty

The temporary nature of immediate expensing introduces uncertainty into the business environment. Businesses engaged in long-term R&D projects require stability and predictability to make informed decisions. The periodic extensions of this policy create a stop-and-start dynamic that disrupts the continuity of ongoing projects, hampering the effectiveness of efforts to drive innovation. Critically, many start-ups and small businesses do not have the resources to keep up with changes in the tax code, and many were caught off guard by the change in R&D expensing. A quote from the Small Software Business Alliance sums up what many startups and small businesses (including those in the clean energy space) faced:

We are now facing difficult choices because of the large, unexpected, and unprecedented tax liability that we face. Many of us have frozen hiring or suspended projects. Some of us are now considering laying off staff or reducing salaries. Others are borrowing to pay our taxes, either from credit cards, personal savings, or lines of credit.

To unlock the full potential of immediate expensing as an engine for green growth, policymakers must recognize the importance of permanence. Making immediate expensing a permanent fixture of the tax code would provide businesses with the confidence and stability needed to undertake ambitious, forward-thinking R&D projects and investments in more energy efficient equipment. This permanence signals a commitment to fostering a culture of innovation that transcends political cycles, allowing businesses to invest in more efficient and cleaner technologies with a long-term perspective.

Immediate Expensing is Good for American Competitiveness and the Environment

Immediate expensing is a powerful tool that, if made permanent, can significantly contribute to the United States’ economic and environmental goals. By making immediate expensing permanent, Congress will provide entrepreneurs and Americans businesses with the certainty they need to drive economic prosperity and environmental stewardship for generations to come.

It Costs More To Permit Infrastructure Than To Build It — But One Lawmaker Wants To Change That

Drew Bonds writes about America’s broken permitting process for the Washington Star. “A project